[ad_1]

Some individuals who critique my numerous price range charts are aggravated I checklist retirement contributions and investments as bills. Due to this fact, I believed I’d clarify my logic on this put up.

When you begin treating your retirement contributions and investments as bills, you’ll start to construct rather more wealth than the common individual. And when you construct extra wealth than the common individual, your frustration will subside, and you’ll really feel extra free.

The hot button is to go from a defensive mindset to an offensive mindset to construct extra wealth. Let’s begin with a fundamental understanding of two monetary statements.

Earnings Assertion: Investments As An Expense

Beneath is a pattern price range of a family making $350,000 a 12 months.

The beneath price range can be seen as an Earnings Assertion. The Earnings Assertion solely has Earnings and Bills. Due to this fact, you will need to categorize any line merchandise that’s not an Earnings as an Expense and vice versa.

Given cash should be spent to contribute to a retirement plan, a 529 plan, a mortgage, and numerous insurance coverage insurance policies, these line gadgets are bills. These bills scale back the underside line, which is the Money Circulation After Bills line in inexperienced.

To remain per the Earnings Assertion analogy, it ought to be labeled as Internet Revenue, as there may be additionally a Money Circulation Assertion in finance. Nevertheless, no person calls the cash they’ve left over as internet revenue.

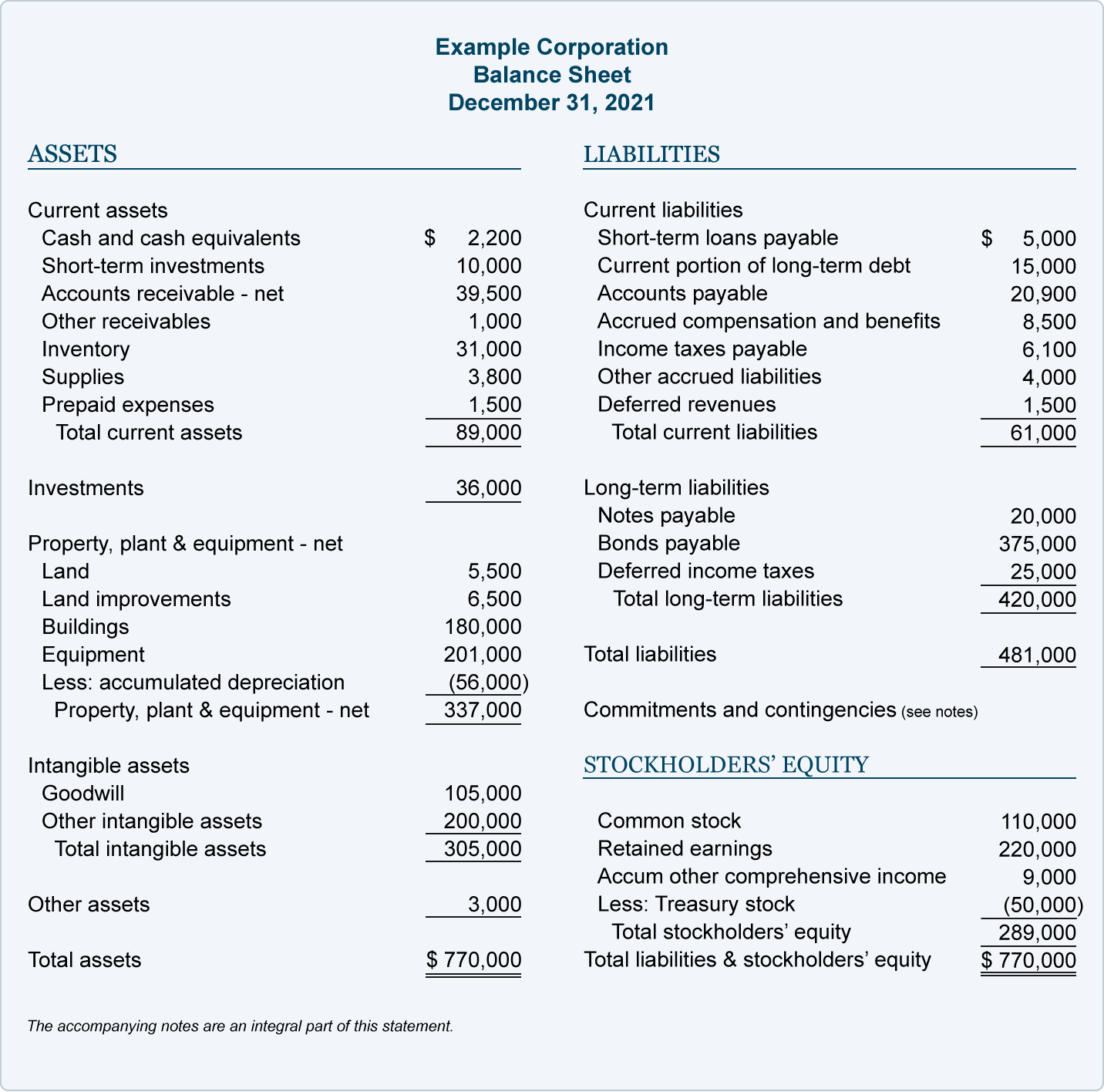

Steadiness Sheet: Investments Are Thought of Belongings

Please don’t confuse an Earnings Assertion with a Steadiness Sheet. A Steadiness Sheet is the place you’ll be able to label all investments and retirement contributions as Belongings. Whereas an Earnings Assertion solely comprises earnings and bills.

A private stability sheet basically calculates one’s Internet Price. And Internet Price is calculated by including up the worth of all Belongings and subtracting the worth of all Liabilities.

Over time, you hope your retirement funds and different investments like actual property develop in worth. In the event that they do, your property and your internet value go up in case your liabilities keep the identical or go down.

Even when your investments are declining in worth, they don’t seem to be thought-about liabilities. Examples of liabilities embrace mortgage debt, bank card debt, cash owed to suppliers, taxes owed, and wages owed.

Beneath is an instance of a Company Steadiness Sheet. You may translate Stockholder’s Fairness into Internet Price if the beneath was a Internet Price Assertion.

Why Individuals Get Bent Out Of Form About Investments As An Expense

Not having a elementary grasp of monetary statements is why most individuals are upset I checklist investments as an expense.

These of us assume I’m making an attempt to trick them into considering a $350,000 family earnings household is poor with solely $19 a month or $224 a 12 months in money circulate left over. No, they don’t seem to be poor. You’re solely tricked by what you see should you don’t perceive what you’re .

On the similar time, critics accurately level out such a household is contributing $41,000 a 12 months of their 401(ok), $26,400 a 12 months of their 529 plans, and constructing $25,200 a 12 months in dwelling fairness. The entire internet value contribution to such bills is roughly $92,700 a 12 months.

As somebody who desires to realize monetary independence, one among your objectives is to reduce taxable earnings and maximize internet value. When you obtain a internet value equal to a minimum of 10X your gross earnings, you’re near monetary independence. As soon as your internet value equals 20X your gross earnings, you’re completely free to do no matter you need.

Problem Investing For The Future

Another excuse why some individuals don’t like treating retirement contributions as an expense is that investing requires self-discipline and delayed gratification. Generally, all you wish to do is spend your cash on residing it up now. Many are logically performing some revenge spending given the pandemic is nicely into its third 12 months.

Due to this fact, it might be onerous for some individuals to conceptualize that in an effort to reside a extra free life in a while, you will need to first spend by investing. Though there aren’t any ensures in investing, traditionally, investments in shares, actual property, and different asset courses do present optimistic returns.

Delayed gratification by way of investing is an expense. You sacrifice good instances now for hopefully good instances later. Those that failed the marshmallow check once they have been younger are seemingly failing the act of saving and investing sufficient for his or her future.

Investments As A Luxurious Expense

Some individuals battle greater than others to outlive. When you find yourself having a troublesome time affording fuel and groceries, it might upset you that others can. In different phrases, investing is seen as a luxurious expense they can not afford.

Nevertheless, deep down, all people is aware of we have to make investments for our future. In any other case, we are going to find yourself working long gone after we are totally succesful or wish to.

So sure, investing is taken into account a luxurious expense for many who are having a harder time making ends meet. Fortunately, investing in shares is now free attributable to zero commissions. We will purchase ETFs and fractional shares with lower than $100. We will even put money into a personal actual property fund with simply $10 to begin by way of Fundrise.

Therefore, investing will not be as massive of a luxurious expense as some may assume. The extra we are able to get educated concerning the energy of investing, the much less we are going to view investing as a luxurious expense and extra as a necessity.

Insurance coverage As An Expense

Most individuals received’t debate whether or not insurance coverage is an expense or not. You’re spending cash to pay for one thing to guard you sooner or later in case of a calamity.

I’ll fortunately pay $115/month for my new 20-year, $750,000 time period life insurance coverage coverage I acquired due to PolicyGenius as a result of I’ve two younger youngsters and mortgage debt. Defending my household over the following 20 years is paramount. As soon as my children are of their 20s, they need to have the ability to fend for themselves. My life insurance coverage premiums are positively an expense.

Due to this fact, why would anyone argue that contributing $41,000 a 12 months to 2 401(ok) plans shouldn’t be thought-about an expense when the contributions are made to deal with the instance family in retirement? Few individuals can and wish to work eternally. I fizzled out earlier than age 35 at a standard day job and faux retired. By the point I’m 50 I in all probability received’t wish to write as a lot both.

If insurance coverage is taken into account an expense to guard your future, then investments must also be thought-about an expense.

Mad About The Quantity Earned And Invested

The ultimate cause why I feel some individuals don’t view retirement contributions and investments as bills is as a result of they’re upset by the quantities I’ve highlighted.

Due to inflation, my $300,000 earnings assertion from a number of years in the past has now jumped to $350,000 at this time. Due to the federal government rising the utmost 401(ok) contribution to $20,500 from $19,500, the whole 401(ok) contribution for 2 is now $41,000 in my chart and never $39,000.

Nevertheless, if I printed a $60,000 family earnings assertion and a $3,000 annual 401(ok) contribution quantity, possibly that may be extra “acceptable.”

Please don’t get fixated on absolutely the greenback quantities. All of us reside in numerous elements of the nation with totally different value of residing requirements and tastes. I’m utilizing these figures as a result of $300,000+ is what it takes to reside a middle-class way of life with two children in San Francisco. In the meantime, I’m at all times a proponent of maxing out your 401(ok).

It was powerful to max out my 401(ok) once I was solely making $40,000 and residing in Manhattan. However I did so as a result of I shared a studio with a good friend. I additionally labored late so I may eat on the free cafeteria every night time. Looking back, the sacrifices have been value it.

Maintain Your Funding Bills Excessive!

I used to be going to conclude by encouraging everybody to maintain their bills low in an effort to quicken their tempo to monetary independence. However then I noticed this was a defensive method to save your method to wealth and freedom. As a substitute, I’m a a lot greater proponent of spending your method to wealth and freedom, which is the subtitle and core idea of my new e-book.

Since we now all agree our investments ought to all be thought-about bills, let me encourage you to maintain your funding bills excessive! Go on the offensive to win extra wealth. This can be a essential mindset shift I encourage everybody to undertake.

On the finish of the day, you need your investments to generate as a lot passive earnings as doable to be free. Relying on the place you’re, your investments could possibly be your largest expense of all of them!

Readers, do you see retirement contributions and investments as bills? If not, why? Why can’t some individuals view investing for his or her future as a gift day expense?

For extra nuanced private finance content material, be part of 50,000+ others and join the free Monetary Samurai publication. Monetary Samurai is among the largest independently-owned private finance websites that began in 2009. To get my posts in your inbox as quickly as they’re printed, enroll right here.

[ad_2]

Leave a Reply