[ad_1]

As you become old, wiser, and begin to earn your individual earnings, your funds develop into much more essential to you. They’ll decide your spending habits, the way you make investments your cash, the place you reside, and extra. In addition to the sum of money you’re incomes and the way you select to spend it, there are different issues which have a considerable affect in your each day life. On this case, we’re speaking about your credit score rating.

However why do you want a credit score rating?

There are numerous the reason why you want a credit score rating. Your credit score rating is a vital quantity that can be utilized to measure your creditworthiness if you apply for a bank card or mortgage, and even if you need to purchase a automobile. A very good credit score rating can provide you extra entry to favorable loans, bank cards, decrease down funds, and a lot extra.

Within the first chapter in our credit score collection, we went over the credit score rating definition and what your credit score rating says about you. However on this chapter, we’ll be answering essential questions like “what’s the purpose of a credit score rating?” and “how can I construct my credit score?”.

To study extra about why you want a credit score rating and its significance in your monetary future, proceed studying the submit or use the hyperlinks under to skip to the part you want.

Why Do We Have a Credit score Rating?

The reply to the query “why do we’ve got a credit score rating?” is definitely fairly easy: Your credit score rating determines the loans you get and the charges you pay. Your credit score rating can severely affect your monetary life, and there are numerous unwanted side effects of bad credit report.

For instance, a very good credit score rating can assist you get a low rate of interest and down fee on a house, however a bad credit report rating would possibly forestall you from getting authorised for the house mortgage in any respect. In case your credit score rating isn’t precisely the place you need it to be proper now, don’t freak out. There are numerous methods you possibly can optimize your credit score rating, and we’ll be discussing credit score constructing ideas in a while within the collection.

Your credit score rating is predicated in your credit score historical past. Based on the Federal Commerce Fee, credit score historical past is outlined as the way in which by which you utilize your cash—what number of bank cards and loans you will have, whether or not or not you pay your payments on time, and many others. Your credit score historical past tells a narrative that provides lenders and different entities perception into your funds. All of this data goes into one thing referred to as a credit score report.

Credit score historical past vs. credit score report

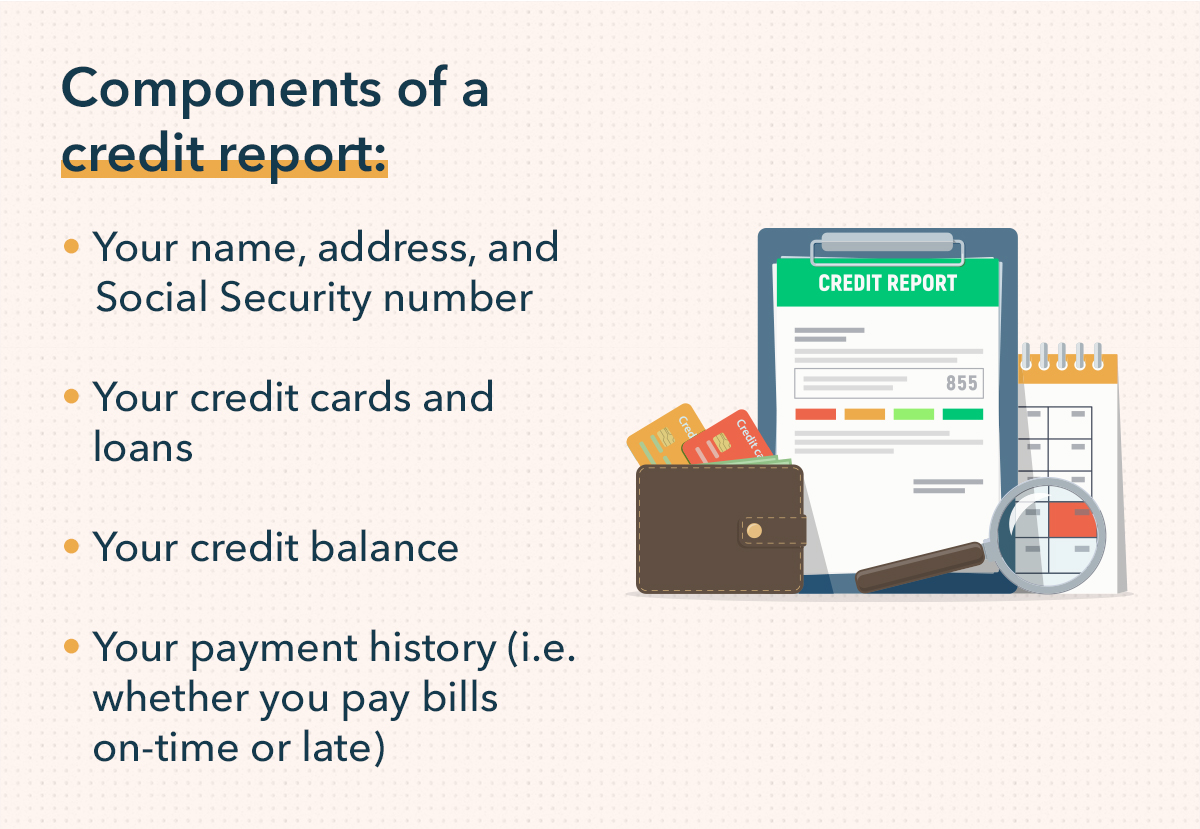

A credit score report is a abstract of your credit score historical past that features data reminiscent of:

- Your title, deal with, and Social Safety quantity

- Your bank cards and loans

- Your credit score stability

- Your fee historical past (i.e. whether or not you pay payments on time or late)

Your credit score report additionally encompasses a quantity, referred to as a credit score rating, that provides a high-level perspective of your credit score well being. Monetary regulators, lenders, and credit score reporting bureaus have assigned classes to distinguish bad credit report scores from common and good credit score scores.

To make issues extra difficult, there are two sorts of credit score scores that lenders and different entities use—FICO and VantageScore. Every of those scores have their very own scoring programs. Let’s check out the completely different credit score scores and what they imply:

- Poor: <580

- Truthful: 580-669

- Good: 670-739

- Very Good: 740-799

- Distinctive: 800+

- Superprime: 781-850

- Prime: 661-780

- Close to prime: 601-660

- Subprime: 300-600

Observe: Intuit makes use of TransUnion VantageScore to offer buyer credit score stories.

The typical credit score rating within the U.S. is round 675, however this varies by age and state. It’s essential that you recognize test your credit score rating in an effort to keep on prime of any adjustments and errors that happen. You also needs to know dispute objects in your credit score report, like in case your title or social safety is unsuitable. You don’t need incorrect data in your credit score report that could possibly be negatively impacting your credit score rating.

Why you want a credit score rating

The best way you handle your credit score accounts, how a lot you’re spending on credit score, and whether or not you pay on-time all contribute to your credit score historical past, and subsequently, your credit score rating. As we alluded to within the introduction, your credit score rating is an important determine in monitoring your monetary wellness. Listed here are just a few the reason why it may be a good suggestion to concentrate on constructing your credit score historical past and establishing good credit score.

Having a very good credit score rating can:

- Make it simpler to open bank cards, loans, and different new strains of credit score

- Allow you to get a greater mortgage fee

- Improve your eligibility for decrease mortgage and bank card charges

- Provide you with higher negotiating energy with lenders

- Pace up the method for residence and condominium leases

- Decrease your automobile insurance coverage charges

Tips on how to test credit score historical past

Now that you just perceive the significance of building a very good credit score historical past, you’re in all probability questioning, “how can I test my credit score historical past report?”.

The regulation states that yearly, you may get a free copy of your credit score report. You may request your credit score historical past report by calling 1-877-322-8228 or visiting AnnualCreditReport.com. Your free credit score report gives you an in depth overview of your credit score historical past, fee historical past, strains of credit score, and extra.

Moreover, you might also contact your financial institution or bank card supplier to see in the event that they embody credit score reporting as a part of your membership plan. Or, get began with Mint to entry your free credit score rating at this time.

Tips on how to Construct Credit score if Your Credit score Historical past is Restricted

One of the simplest ways to ascertain a very good credit score historical past is slowly, over time. Make funds on time. Repay balances as you go, or at the very least hold them moderately low. Maintain your debt to credit score ratio low. Because the years go by, all of your accountable habits can assist you construct a very good credit score historical past.

You say you possibly can’t wait to get began? Let’s check out seven ideas for constructing credit score in an effort to elevate your credit score rating as shortly as doable:

1. Contemplate a secured bank card

Even in case you have a brief credit score historical past, you should still be capable of qualify for a secured bank card. For any such bank card, you deposit money that serves as your credit score restrict.

Contemplate any charges and costs when deciding between secured playing cards. And make sure the cardboard you select stories your account exercise to the key credit score bureaus together with TransUnion®. Not all playing cards do that, so that you need one which highlights your nice observe report.

2. Ask about credit score the place you financial institution, store, or get gasoline

If you have already got a financial savings or checking account, your financial institution could approve you for a card with a low credit score restrict.

You too can attempt making use of for a gasoline bank card or retailer bank card. These normally have smaller credit score limits, however it’s usually simpler to qualify for them. Fuel bank cards are normally good at just one chain of gasoline stations, however you possibly can reap the benefits of reductions and perks. Retailer bank cards are additionally restricted, however they usually provide rewards like cashback, factors for sure purchases, or advantages like free delivery.

3. Discuss to lenders earlier than you apply

For individuals with out lengthy credit score histories, some lenders could look at knowledge from much less conventional sources, like utility or rental funds. In case your credit score historical past is comparatively transient, it’s completely acceptable to ask your lender in the event that they’ll take a look at different knowledge after they’re contemplating your utility. Simply do it earlier than you apply—asking after you’ve been denied could also be much less efficient.

4. Look right into a credit score builder mortgage

This works on the identical precept as a secured bank card, besides it’s a mortgage.

Right here’s an instance of the way it works. Let’s say you are taking out a small mortgage from a financial institution after which use that mortgage to open one in all their Certificates of Deposit (CDs). The financial institution holds the CD, when you make common funds on the mortgage. If you’ve paid off your mortgage, you personal the CD. You find yourself with some financial savings, plus a very good credit score observe report.

The draw back? Any curiosity and costs it’s important to pay on the mortgage. Ensure you select a lender that may report your on-time funds to the three main credit score bureaus. And attempt to discover a financial institution that gives low charges and costs.

It’s additionally essential to concentrate on the professionals and cons of paying off a mortgage early. Paying off a mortgage early means you’ll be in much less debt and also you’ll pay much less on curiosity, however it will probably additionally probably decrease your credit score rating if it’s the one mortgage account you will have. So earlier than you go forward and repay the mortgage in full, perform a little research to determine if it’s the appropriate selection for you.

5. Develop into a certified consumer

You may ask somebody (normally a member of the family or shut pal) so as to add you as a certified consumer on their bank card. That approach, the account’s historical past will probably be added to your credit score report.

In fact, you’ll need to select an individual whose account is in good standing. There’s all the time the chance that they might miss funds, find yourself in collections, and even go bankrupt. In that case, their dangerous habits may harm your credit score report. So, in the event you do develop into a certified consumer, monitor your credit score report to make sure there are not any points and funds are being made on time.

6. Don’t apply for a number of bank cards without delay

Making use of for plenty of bank cards unexpectedly could appear to be a great way to kickstart your credit score historical past, however it will probably really harm your credit score and lift alarm bells for card issuers. Be selective. Search for the most effective charges from manufacturers you recognize.

7. Watch out about closing accounts

If you lastly repay a bank card invoice, you is likely to be tempted to instantly discover out repair a closed account. However eliminating a closed account isn’t all the time the appropriate choice in the case of your credit score historical past.

Closing credit score accounts could considerably shorten your credit score historical past. Accounts you shut will ultimately cease showing in your credit score stories and received’t be calculated in your credit score rating.

Right here’s an instance:

Let’s say you will have two bank cards: one with a $20,000 credit score restrict and 0 stability and one other card with a $10,000 restrict and a $5,000 stability. If you happen to resolve to shut the $20,000 restrict card since you not use it, this will likely negatively have an effect on your utilization ratio (the quantity of debt you’re utilizing in comparison with the quantity you will have obtainable), your credit score rating and your credit score historical past. So except a card has excessive charges, contemplate leaving it open. Make just a few small purchases occasionally and pay them off month-to-month.

Key Takeaways: Why Do You Want a Credit score Rating?

Constructing your credit score historical past is a vital step to absorb managing your funds. Earlier than you go off to construct your credit score historical past and begin working towards good credit score habits, hold these key takeaways in thoughts:

- The place can I test my credit score report? You may entry a free credit score report every year by way of AnnualCreditReport.com, or request your free credit score rating with Mint at this time.

- Does a credit score report present credit score rating? Sure, your credit score report will characteristic essential metrics relating to your credit score historical past. This will embody your credit score rating, figuring out data, fee historical past, and extra.

- Do I want a bank card to ascertain a credit score historical past? Opening a bank card is a good way to start out constructing your credit score, however there are different choices that may allow you to get began. Secured bank cards, retailer bank cards, credit score builder loans, and changing into a certified consumer on a relative’s account are just a few examples to contemplate.

Your Credit score Rating Is Important to Monetary Wellness

With the above in thoughts, you possibly can see why your credit score rating is so essential and why it ought to all the time be prime of thoughts in the case of your monetary well being. So now that you recognize the reply to the query “why do you want a credit score rating?”, you possibly can transfer onto the following chapter within the collection, the place we’ll be discussing the assorted components that have an effect on your credit score rating.

Begin retaining observe of your price range and total monetary wellness by studying extra about Mint at this time.

Browse Associated Articles

[ad_2]

Leave a Reply