[ad_1]

Step one for Amy is to enhance her tax effectivity, professional says

Evaluations and suggestions are unbiased and merchandise are independently chosen. Postmedia might earn an affiliate fee from purchases made via hyperlinks on this web page.

Article content material

In Ontario, a lady we’ll name Amy, 57, works for a neighborhood group. She has no dependents and only one debt of $25,000 used to purchase an funding. Her monetary aim is a sustainable $40,000 per yr — or $3,333 per 30 days — in after-tax revenue when she retires at age 60. That’s roughly her current spending minus financial savings and mortgage compensation.

Commercial

This commercial has not loaded but, however your article continues under.

Article content material

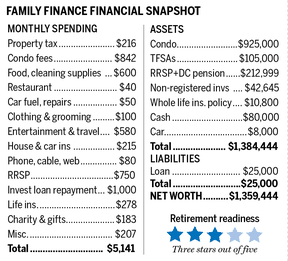

Household Finance requested Derek Moran, head of Smarter Monetary Planning Ltd. in Kelowna, B.C., to work with Amy. He notes that she has $1,384,444 of whole property together with her apartment. That sum contains $451,444 of economic property together with $80,000 money. Her web price is $1,359,444. Her funding portfolio is essentially an inventory of high-fee, principally fixed-income mutual funds.

Article content material

E mail andrew.allentuck@gmail.com for a free Household Finance evaluation

A decade in the past, Amy made a big funding in an RRSP-eligible mortgage firm that inspired savers to dip deeply into their financial savings. She made an enormous wager on the enterprise and misplaced $211,000, which was 70 per cent of her RRSP’s worth on the time.

“I knew property was hovering and it appeared like a method to get in on it,” she recollects. She gambled on what she believed to be a positive factor. The one positive factor was the fats incomes for funding managers and salespeople. Her response has been to put money into low-return property that don’t tempo inflation.

Commercial

This commercial has not loaded but, however your article continues under.

Article content material

Present investments

As we speak, Amy has a month-to-month funds of $5,141, of which $1,750 goes to financial savings and the compensation for an funding mortgage. That leaves true spending at $3,391 per 30 days or $40,692 per yr. To generate that quantity after tax, Amy would wish $48,000 per yr earlier than tax.

Step one for Amy is to enhance her tax effectivity. She has $104,954 of RRSP contribution area. She generates an additional 18 per cent of wage for RRSP area, which works out to $17,159 per yr. For 4 years, that provides as much as $68,636. Mixed along with her current RRSP room, she will add as a lot as $173,590 with out over-contributing. She will be able to get a 30 per cent tax refund for any RRSP contributions she makes whereas working however will most likely need to pay tax at not more than 15 per cent when she takes the cash out in retirement.

Commercial

This commercial has not loaded but, however your article continues under.

Article content material

She additionally has a supply of cash in a complete life insurance coverage coverage with $50,000 face worth and $10,800 of money worth. She has no youngsters to whom to depart cash, so she might money out the coverage and use the money worth for the RRSP or donate the coverage to a charity for a tax profit. Her current spending contains $278 month-to-month for entire life protection.

Sources of retirement revenue

We’ll estimate that Amy will get 90 per cent of the current most CPP profit $15,043, web $13,500 per yr. She will even get full Outdated Age Safety, presently $7,707 per yr.

Her TFSA has a gift stability of $105,000. The TFSA stability rising at three per cent per yr after inflation will likely be $118,178 in 2022 {dollars} when she is 60. Spent over the next 30 years to her age 90, that sum would assist spending of $5,979 per yr.

Commercial

This commercial has not loaded but, however your article continues under.

Article content material

Amy’s RRSP and LIRA, together with her work-based defined-contribution plan, whole $212,999.

Amy’s aim needs to be to make use of the RRSP to carry her taxable revenue all the way down to $49,020 which is the highest of the primary federal tax bracket. That manner, she is going to optimize her tax refund. A number of the contribution might be deferred and deducted subsequent yr, Moran explains. Refunds can return to her financial savings.

-

A kitchen reno put a dent on this Alberta trainer’s TFSA. Now she has to play catch up for retirement

-

Father awarded greater than $675,000 in prices after epic five-year battle over youngsters

-

This Ontario lady ought to shed actual property and debt to satisfy her retirement revenue aim

If Amy diverts all month-to-month financial savings, $1,750 plus $397 from her employer, for a complete of $2,147 per 30 days or $25,764 per yr over 4 years, plus contributes $70,000 from her present money holdings, the RRSP may have have risen to about $430,000. If she additionally contributes the $66,000 in tax refunds she generates over that interval, it would depart her with near $500,000.

Commercial

This commercial has not loaded but, however your article continues under.

Article content material

These funds rising at three per cent per yr for the next 30 years will assist a taxable revenue of $25,096 per yr.

Earlier than age 65, Amy may have TFSA money move of $5,979 per yr and RRSP revenue of $25,096, whole $31,075. After 12 per cent common tax excluding TFSA revenue, she may have $28,060 per yr to spend. She would come up considerably wanting her after-tax goal revenue. Choices to shut the hole included part-time work or downsizing from her $1-million apartment to a $500,000 unit and utilizing money, say $12,000 for 5 years to age 65, to remain within the black. It could permit her so as to add to her monetary property and their income-producing potential.

Swapping property for revenue

Rebalancing to make her dwelling, a smaller apartment maybe, only a third of whole property would liberate worth for funding, notably shares that pay strong dividends of three per cent to 4 per cent a yr issued by firms which have a historical past of elevating payouts. Lists of those dividend aristocrats are available on-line.

Commercial

This commercial has not loaded but, however your article continues under.

Article content material

The apartment sale yield can be lowered by preparation and promoting prices at 5 per cent of worth, however the remaining stability $878,750 much less $500,000 for brand new digs, would depart $378,750 for bills and funding. Invested at three per cent after inflation, that capital’s everlasting revenue can be $11,362 per yr or $947 per 30 days. Her whole annual revenue would rise to about $42,400 earlier than tax. After 13 per cent tax that would depart her about $37,675 per yr or $3,140 per 30 days to spend. She would nonetheless be under goal. Half-time work would shut the hole to her $40,000 after tax goal.

As soon as she is 65, Amy can add $13,500 CPP per yr and $7,707 OAS for whole estimated annual revenue of $52,282. After 15 per cent, she would have $45,337 to spend annually. That’s $3,780 per 30 days. Amy would exceed her after tax money month-to-month retirement goal of $3,333.

3 Retirement Stars***out of 5

e-mail andrew.allentuck@gmail.com for a free Household Finance evaluation

Commercial

This commercial has not loaded but, however your article continues under.

[ad_2]

Leave a Reply