[ad_1]

Tom and Charlene should rely upon financial savings to make retirement work, skilled says

Evaluations and suggestions are unbiased and merchandise are independently chosen. Postmedia might earn an affiliate fee from purchases made by way of hyperlinks on this web page.

Article content material

A pair we’ll name Tom and Charlene, each 40, dwell in B.C. with their seven-year-old son Sam. They bring about house $13,179 monthly from their jobs in excessive tech plus further revenue from a rental property. Tom has a defined-benefit pension, however retirement at 55, which is their aim, would imply a discount within the annual payout. Their query is when to begin retirement: the sooner they retire, the longer their should carry the chance {that a} rising price of residing will eat away at their shopping for energy. For a retirement may final 35 years, that threat is substantial.

Commercial

This commercial has not loaded but, however your article continues beneath.

Article content material

The pension wouldn’t be the one revenue stream in danger from an early retirement. Stopping work may additionally lower into earnings wanted to generate CPP advantages by about 15 to twenty per cent. That’s on prime of the 36-per-cent discount that might come from beginning CPP at 60.

The monetary query is: Can they make their plan work and obtain their aim of $6,000 in minimal month-to-month revenue?

Article content material

E-mail andrew.allentuck@gmail.com for a free Household Finance evaluation.

Household Finance requested Derek Moran, head of Smarter Monetary Planning Ltd. in Kelowna, B.C., to work with Tom and Charlene.

Earlier than going any additional, the couple desires to make sure they’ve offered for post-secondary training for Sam. He has $30,000 in his RESP. The dad and mom contribute $208 monthly and obtain the lesser of 20 per cent or $500 per yr from the Canada Training Financial savings Grant to a $7,200 restrict per beneficiary. Assuming three per cent annual progress of rising balances, at 17, when prepared for post-secondary training, Sam may have $62,500. That’s enough for a four-year diploma if he lives at house.

Commercial

This commercial has not loaded but, however your article continues beneath.

Article content material

The monetary base for retirement

To make retirement work with a begin a decade earlier than the same old begin of CPP, OAS and firm pensions, Tom and Charlene should rely upon financial savings.

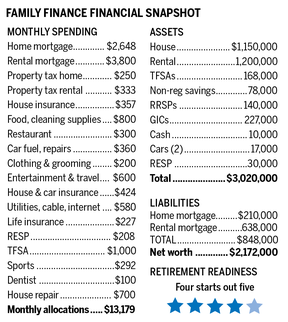

They’ve $227,000 in GICs and $10,000 in money they will use so as to add to RRSPs to scale back taxes and maybe for discount of their two main money owed — $210,000 on their home and $638,000 on their rental.

For now, the couple’s web value, $2,142,000, is superb for his or her ages, Moran explains. They’ve enough financial savings to create tax-reduction alternatives. Every companion has unused RRSP room: $125,000 for Tom and $78,000 for Charlene. They need to take $67,000 from their GIC and put it into Tom’s RRSP to chop his taxes. They will use the remaining $160,000 money to pay down their $210,000 private mortgage to only $50,000. Reamortize the house mortgage over 10 years to a small fee of $462 monthly and divert $2,186 monthly from the previous $2,648 former quantity to the RRSP.

Commercial

This commercial has not loaded but, however your article continues beneath.

Article content material

Pension math

Tom’s work pensions can pay him $59,724 per yr if he works till he turns 62, however yearly earlier than that may end in reductions, due each to having fewer years of labor credit score and the sooner begin date. At 55, he would qualify for $25,060 per yr, lower than half of the age 62 degree.

The present most payout for CPP is $14,445 per yr. The loss brought on by quitting at 55, because of a discount in years labored, a key a part of the CPP formulation, can be 15 per cent for Tom and 30 per cent for Charlene. That reduces their base age-65 CPP funds to $12,278 and $10,112, respectively.

Every companion will have the ability to take full Outdated Age Safety, at the moment $7,707 per yr, at 65.

The couple’s RRSPs have a gift whole of $140,000. A one-time contribution of $67,000 plus $2,186 monthly rising at three per cent after inflation for 15 years to retirement would change into $825,023 at age 55. If that sum is spent over the next 35 years, it could present $37,278 pre-tax annual revenue, all in 2022 {dollars}.

Commercial

This commercial has not loaded but, however your article continues beneath.

Article content material

The couple’s $168,000 TFSA stability plus $12,000 annual contributions rising at three per cent over the speed of inflation would change into $491,620 at retirement in 15 years. That capital, spent over the next 35 years to their age 90 would generate $22,213 per yr to the exhaustion of all revenue and capital.

-

This couple desires to retire at 60, however wants to hurry up their financial savings to get there

-

B.C. couple has important mortgage debt heading into retirement, however threat ought to diminish with time

-

Pensions and money from a cottage sale put this Ontario couple’s retirement on stable floor

Their $1.2 million rental is a dilemma. It produces lease of $5,000 monthly. They’ve $562,000 fairness and owe $638,000. Property tax, insurance coverage and the curiosity on the mortgage price them $18,311 per yr. Their web rental revenue, $60,000 much less prices, leaves them with a wholesome $41,689 per yr. They’ve a gift seven per cent return on fairness, which is superb. If they can absolutely pay down the rental mortgage by 55 — it will likely be shut — they might haven’t any mortgage curiosity and due to this fact $50,812 annual web lease.

Commercial

This commercial has not loaded but, however your article continues beneath.

Article content material

At 55, the couple would have $37,278 from RRSPs, $22,213 from TFSAs and $50,812 lease with mortgage paid and Tom’s $25,060 pension. That’s a complete of $135,253. Assuming splits of eligible revenue, no tax on TFSA revenue and 19 per cent common tax, then with TFSA money circulation restored, they might have $9,480 to spend monthly. At 65, they might add $12,712 and $10,112 from CPP and $7,707 per particular person from OAS, whole $173,450. With splits, no tax on TFSA money circulation, and 20 per cent common tax they might have $11,935 monthly to spend. Their goal minimal retirement revenue, $6,000 monthly, can be attained and can be sustainable. With no mortgage fee for house or rental and no RESP or TFSA financial savings, their prices would drop by $7,656 to $5,523 monthly.

Dangers

Early retirement implies that if inflation picks up, the corporate pension will lose buying energy and rates of interest will are likely to rise. We will’t predict inflation charges, however the threat to revenue is obvious. Had been Tom to work to 62, he may lock in a a lot bigger annual pension fee, and mitigate these inflation dangers.

Retirement stars: 4 **** out of 5

E-mail andrew.allentuck@gmail.com for a free Household Finance evaluation.

Commercial

This commercial has not loaded but, however your article continues beneath.

[ad_2]

Leave a Reply