[ad_1]

Ron and Mary would have greater than sufficient to fulfill their modest objectives, professional says

Critiques and suggestions are unbiased and merchandise are independently chosen. Postmedia could earn an affiliate fee from purchases made by means of hyperlinks on this web page.

Article content material

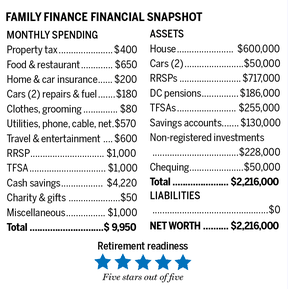

In Alberta, a pair we’ll name Ron and Mary, ages 49 and 45, are taking an extended have a look at the top of their respective careers in equipment gross sales and highway administration. Ron has put in 30 years together with his firm and earns a gross annual earnings of $90,000. Mary, a frontrunner in her area of interest of the development supplies trade, has 17 years along with her firm and earns $69,000 per 12 months earlier than tax. They take residence $9,950 monthly.

Commercial 2

Article content material

They need to know if they will each retire in six years with a mixed annual earnings of $60,000 after tax. However they’re additionally contemplating a second possibility, which might see Ron retire instantly and Mary work for an additional decade.

e-mail andrew.allentuck@gmail.com for a free Household Finance evaluation

Household Finance requested Eliott Einarson, a monetary planner who heads the Winnipeg workplace of Ottawa-based funding advisory agency Exponent Funding Administration Inc., to work with Ron and Mary.

Article content material

Calculating their property

Ron and Mary each have defined-contribution matching plan to which every contributes three per cent of gross pay equalled by employers and which due to this fact develop at six per cent plus funding returns. Every month they save $1,000 for his or her RRSPs and $1,000 mixed monthly to their TFSAs. $4,220 month-to-month goes to non-registered financial savings.

Commercial 3

Article content material

Their property thus embrace their residence, valued at $600,000, which they’ve absolutely paid for; two DC pensions value a complete of $186,000; $255,000 of their TFSA accounts; RRSPs with a stability of $717,000; $130,000 in so-called high-interest financial savings account; and non-registered accounts with a stability of $228,000. Throw within the $50,000 worth of two vehicles and $50,000 of their chequing accounts and their current web value is $2,216,000.

Staggering their retirements

If Ron have been to retire this 12 months at 49 and Mary continued to work to 55, as they’ve thought of, they would want $45,000 per 12 months after tax for primary spending. Mary’s $3,800 month-to-month after-tax earnings could be sufficient to cowl them. However what would occur when Mary retires?

Commercial 4

Article content material

With no additional financial savings to registered or different accounts, Ron’s $510,000 in registered investments, together with his $84,000 defined-contribution pension plan, left to develop at three per cent per 12 months after inflation would rise to a price of $685,400 in ten years when Mary could be 55 and would retire.

That sum would offer Ron $30,480 per 12 months for the next 36 years on the similar charge of progress and distribution of all capital earnings. The funds would run out when Ron is 95 and Mary is 91.

Ron’s non-registered property and financial savings held in joint identify with Mary with a complete worth of $330,000, rising at three per cent after inflation for ten years, would rise to a price of $443,500. That sum would offer $19,722 annual earnings to his age 95. His DC pension and half this joint non-registered earnings, $9,861, would offer Ron an earnings of $40,340 in 2022 {dollars}.

Commercial 5

Article content material

Mary’s $393,000 of registered property together with $102,000 in her DC pension plan with annual matching contributions would develop to a price of $577,043 in ten years. That sum would generate earnings of $25,660 per 12 months for the next 36 years to her age 91. Including in half their joint funding earnings, $9,861, would offer Mary a complete earnings of $35,522 at her age 55. Their complete annual earnings could be $75,860. After splits and 13 per cent common tax, they’d have $66,000 per 12 months or $5,500 monthly, proper on course.

Synchronizing their retirements

Alternatively, they might each proceed to work for an additional six years to his age 55 and her age 51, shortening her time so as to add to property, however extending his.

On this state of affairs, his $510,000 would rise to a price of $644,944 in six years. That might generate $27,079 per 12 months for 40 years. The non-registered investments and financial savings account with a mixed $330,000 worth rising for six years with $3,000 month-to-month additions would have a price of $633,886. That sum would offer every companion half of $26,625 or $13,313 per 12 months to his age 95, giving Ron complete earnings of $40,392 in 2022 {dollars}.

Commercial 6

Article content material

Mary’s registered property would develop to a price of $496,845 by her age 51 with the identical assumptions. This capital would generate $20,865 per 12 months to her age 91. Including in her half of non-registered earnings, $13,312 would give her gross earnings of $34,177. Their complete earnings at this level could be $74,570 firstly of Ron’s retirement in six years. After cut up of eligible earnings and 12 per cent common tax, they’d have $65,621 or $5,470 monthly.

Boosts from TFSAs, CPP and OAS

Their TFSA accounts with a present stability of $255,000 rising with no additional contributions would have a price of $384,432 in six years assuming contributions proceed at $12,000 complete for each for six years. The accounts could possibly be a buffer for surprising bills or they might take the cash out over the next 40 years at $16,364 yearly for journey or different makes use of.

Commercial 7

Article content material

Within the first case — Ron retires at 49 — earnings would rise to $82,364 or $6,865 monthly. Within the second case, annual earnings could be $81,985 per 12 months or $6,830 monthly. We’ll common it at $82,174 or $6,850 monthly.

-

Commuting her pension might let this Ottawa civil servant have her cake and eat it, too. However is it definitely worth the threat?

-

B.C. couple has 5 leases however does not personal their very own residence — and that is an issue for retirement

-

This B.C. couple of their 40s has $3.1 million in property, however is it sufficient to retire in 5 years?

At every companion’s age of 65, Canada Pension Plan and Outdated Age Safety advantages could be accessible. Contribution charges and payouts are altering, however we estimate every companion would have 75 per cent of potential CPP payouts or $10,838 at 65. At 65, every would have OAS advantages of $7,707 per 12 months per individual at 2022 charges. That’s an annual complete of $18,545 every or $1,360 monthly after 12 per cent tax on high of different earnings when every companion reaches 65. Complete month-to-month earnings would rise to $8,225 when Ron is 65 and $9,585 when Mary is 65.

They’d have greater than sufficient to fulfill their modest objectives.

Retirement stars: 5 retirement stars ***** out of 5

Monetary Submit

e-mail andrew.allentuck@gmail.com for a free Household Finance evaluation

Commercial

[ad_2]

Leave a Reply